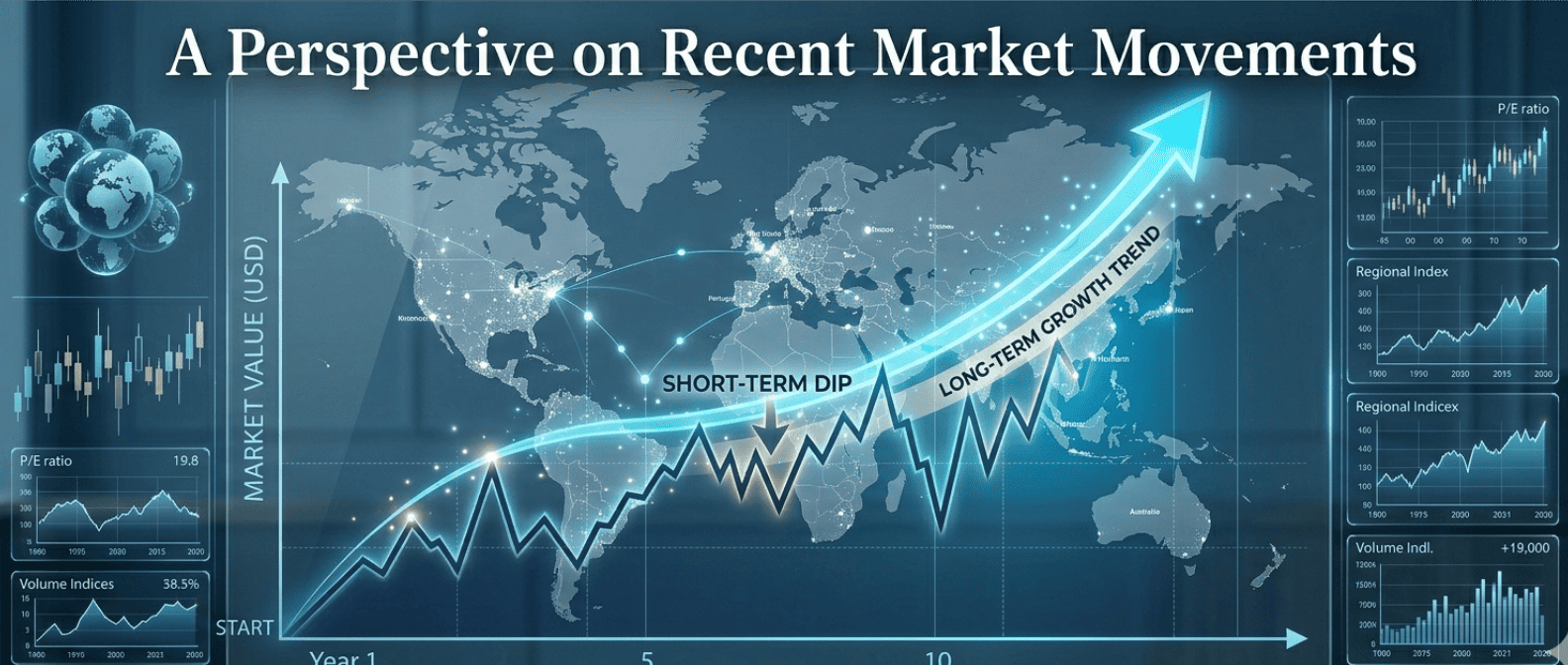

India is benefiting from multiple reinforcing forces—from strong domestic fundamentals and manufacturing growth to digital leadership and rising global strategic importance. While short-term market sentiment will continue to fluctuate, the long-term investment case for India remains compelling, particularly when combined with prudent global diversification.